- Call Us: (800) 565-1722

- How Reverse Mortgages Work

- Reverse Mortgage Pros and Cons

- Consider Downsides

- All Reverse Mortgage Calculator

- Free HECM Calculator (No Personal Info)

- Amortization Calculator

- Purchase Calculator

- 2024 Lending Limits

- Today's Reverse Mortgage Rates

- Counseling Locator

- 3 Types of Reverse Mortgages

- Home Equity Conversion Mortgage

- Jumbo Reverse Mortgage

- Purchase Reverse Mortgage

- Top 20 Reverse Mortgage Lenders

- Search by City or State

- Ask ARLO ™

- ARLO ™ Blog

- ARLO ™ Articles

America’s #1 Rated Reverse Lender

In your current area 100 homeowners are currently utilizing reverse mortgages to better enhance their retirement years, with 500,000 nationwide, great it looks like your home value estimate is about, please provide your estimated home value, the minimum qualifying age for a reverse mortgage is 55, great news your arlo ™ analysis is ready.

- Side-by-side loan comparisons

- Real-time interest rates

- ARLO™ advice to help you select the right program

What to Expect When Your Reverse Mortgage is Assigned to HUD

We received a notice that our reverse mortgage loan is being assigned to HUD, along with the name of the handling company. This company has numerous complaints, especially about foreclosing before heirs can settle the home. I am the beneficiary of my mom’s house, which is in a trust and a will to avoid probate. What recourse do I have if they refuse to work with me and foreclose despite my efforts? The complaints mention lies, runarounds, no payoff amounts, and unreturned calls. This is terrifying, as there’s enough equity to sell the house and pay off the loan. I don’t want to hire an attorney if I’m following all requirements and they still refuse to cooperate. Who can I complain to, and why is this company still in business? My mother, who has the reverse mortgage, is still alive but may not have much longer. Why do they make settling the loan so difficult? -Thank you, Laura K.

Why Lenders Assign Reverse Mortgages to HUD

Let’s start with some background.

Reverse mortgages are typically assigned to HUD when the loan amount is very high compared to the original value or maximum claim amount. The HUD manual mentions other reasons for assignment, but this is the most common one.

Many homes that reach this point have little to no equity left because borrowers have used all the funds available to them, and the interest has accrued on the loan. This is the purpose of a reverse mortgage: it allows borrowers to live in the property without making payments.

If borrowers can afford to make monthly payments to keep equity in the property, they can do so with a reverse mortgage. However, most borrowers choose a reverse mortgage to live in their home without making payments.

Once the borrowers no longer live in the home, HUD’s servicer will move quickly toward foreclosure to minimize losses if they believe the heirs are not actively working to pay off the loan.

Timing of Reverse Mortgage Assignments to HUD

Most reverse mortgages are assigned to HUD when there is little equity left in the property. The longer they wait, the more losses they will incur. Ideally, HUD prefers that heirs pay off the loans, but this is not common when there is little equity.

HUD will contact an appraiser to assess the property’s value. If there is no equity and no one has transferred the title from the deceased borrowers, it is clear that no one is making an effort to repay the loan promptly.

Reverse mortgage lenders and servicers have been sued for releasing information to unauthorized individuals. They can only release information if they have written consent from the borrower, a court order, or a trust with a certified successor trustee.

If someone contacts them without proper authorization, they cannot release any information. This is not the lender or HUD being difficult; it is the law and a result of previous lawsuits.

To avoid issues, make sure everything is in order ahead of time. I have overseen a few reverse mortgage payoffs (including settling my own mother’s loan), and they went smoothly.

Here’s what you need to do:

Setting Up Authority with the Servicer

Ensure you have the authority to speak with the lender on behalf of the loan. This can be done now by having your parents sign an authorization form, allowing the lender or servicer to communicate with the heirs they designate. With this authorization in place, the lender can discuss all loan-related matters with the designated heirs.

This applies to all heirs and must be done in advance. It’s too late to have Mom and Dad sign an authorization after they pass away or become incapacitated.

Ensuring the Trust is in Order

If your mom has a family trust , speak to your estate attorney now and devise a plan to complete the certification of the trust as soon as possible after your mom passes. If your mom is incapacitated, the trust may contain language allowing you to be moved from successor trustee to trustee immediately so you do not have to wait.

Either way, when your mom passes, you will already be the new trustee, with the power to sell the property or take out a new loan without delay.

Neither HUD nor the servicer wants to foreclose. However, they cannot speak to anyone who is not authorized to communicate on behalf of the borrower or show proof of being the new owner. This process usually takes time if you have to go through probate or if heirs do not take immediate steps to change the title after the borrowers pass.

Often, heirs start contacting the lender without proper authorization, leading to frustration and negative comments you may have read. If you have taken the necessary steps to change the title and have the trust certification showing you are now the trustee, the servicer can and will work with you to sell the home.

If you are not recognized as authorized to communicate and act on the borrowers’ behalf, and the title is still in the borrowers’ names (the estate) with no moves being made to change that, the foreclosure action will eventually begin in accordance with the loan terms, especially if there is no equity left in the property to minimize losses.

I recommend taking the steps outlined above: get a signed authorization from your mom if she is capable, or move to position yourself as the trustee of the trust if you are the successor trustee. This will make dealing with the reverse mortgage much easier.

Consulting with an Attorney

As always, I strongly recommend that you speak to your estate attorney who handled the will and trust and get legal advice on any tax or other estate implications before taking any action.

If you ensure that your title and authorizations are in order in advance, you will likely find the process much easier than you have been led to believe.

ARLO recommends these helpful resources:

- Reverse Mortgage After Death: What Heirs & Family Must Know

- HUD Servicing Manual .PDF (4235.1 REV-1 )

Have a Question About Reverse Mortgages?

Leave a reply to this article.

Announcing the 2024 Tech Trendsetters winners.

- Your Account

- Subscription Overview

- Newsletters

- Company Search

Servicing: Assignments to HUD, Part I: Reasons, Processes and Purpose

- Click to share on Twitter (Opens in new window)

- Click to share on Facebook (Opens in new window)

- Click to share on LinkedIn (Opens in new window)

- Click to email a link to a friend (Opens in new window)

- Click to share on SMS (Opens in new window)

- Click to copy link (Opens in new window)

Whether you are involved in reverse mortgage loan servicing, origination or any aspect in between, no doubt you understand and strongly believe in the benefits a reverse mortgage provides to our borrowers. I’m not sure, however, that the industry as a whole understands or appreciates the important role HUD serves with the HECM product. In this two-part piece, the detailed process and aspects of the HUD assignment process will be explored.

Those on the servicing side understand the importance of HUD insurance through its second mortgage and the twofold purpose it serves:

ONE || This second mortgage insures borrowers in the exceptionally unlikely and rare event a lender goes out of business, and

TWO || HUD provides insurance for servicers in the event a loan is not paid back in full. This remedy is essentially handled like any insurance claim, and like traditional insurance, there are different types of claims.

With traditional insurance (auto, home), the most common claims are made when something negative (accidents, injury) happens. I categorize these types of claims in the HECM insurance world as those that are filed for reasons of default. Examples would be when a loan is called due and payable or the loan has been satisfied in any way other than full payment to the lender. These are HUD Claim Type 21 (Foreclosure/Deed in Lieu) and Claim Type 23 (Mortgagor’s Short Sale) processes. Insurance companies also offer incentives for positive records (that is, spotless driving records with no accidents or injuries). In the HECM insurance world, these would include the Assignment to HUD or HUD Claim Type 22 process.

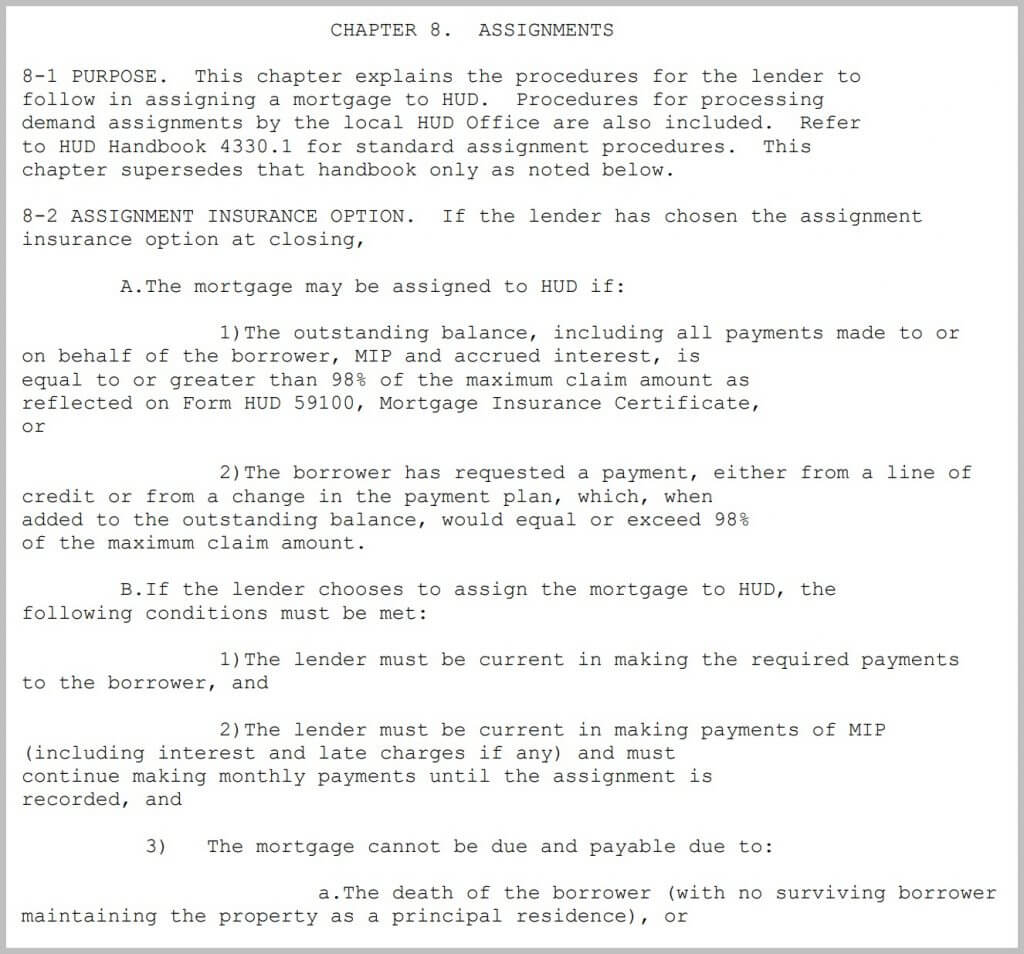

Let’s walk through the complicated territory servicers navigate when a loan reaches 98 percent of its Maximum Claim Amount (MCA), determined by the current loan balance as a percentage of the MCA. The MCA is determined at closing and is defined by HUD as “the lesser of a home’s appraised value or the maximum loan limit that can be insured by FHA.”

When a loan becomes eligible for assignment to HUD at 98 percent of MCA, it must meet certain criteria for

HUD to accept it, take over the servicing and then pay the claim to the lender. To ensure that a loan is ready for this assignment, this criterion is triple-checked well before the balance reaches 98 percent (typically this happens when it approaches 85 to 90 percent). Loans move (slowly) to MCA through the monthly accumulation of interest, mortgage insurance premiums and servicing fees. During this initial review, the servicer is seeking to confirm that the loan is in “active” status.

HUD will not accept a loan for assignment if it is in default or is due and payable. The review focuses on origination documents and ensures that there are no errors on the mortgage, that assignments (if applicable) are in place, and that the servicer has all of the documents required for submission to HUD. If anything is incorrect or out of place in the servicing file, we work aggressively to correct it. As a subservicer, Celink reaches out to its clients involved in the origination process. Rare cases arise when a client (or its subservicer) is unable to fix a document error, which makes the loan’s assignment to HUD impossible.

There may be other reviews of a loan, especially if work is required to complete or fix errors. In short, a final review process follows and this happens much closer to eligibility, around 96-97 percent of MCA. Loans can take years to move to this assignment process.

A majority of loans are paid off or will have moved to default/due and payable status before reaching HUD assignment eligibility. A loan that is eligible at 95 or 96 percent may not be eligible at 97.5 or 98 percent. Additionally, a loan that has lender/force-placed insurance (FPI) or delinquent property taxes is not eligible for assignment. This is true even when the FPI or delinquent property taxes do not create a default status on the loan.

Part II will focus on eligible loans for assignment to HUD and the process of assignment within HUD’s servicing software, HERMIT.

Most Popular Articles

Latest articles.

Leasehold estates, manufactured homes and mortgage fraud are the key topics in the latest Fannie Mae Selling Guide update.

Longbridge parent posts softer Q3 earnings while touting proprietary reverse performance

How will a gop-controlled government impact retirement policy , ginger bell and fobby naghmi on leadership deficits in the mortgage industry , trump tariffs would result in homebuilder price increases , will trump, project 2025 kill hud .

Remember me

Don't have an account? Please Sign Up

IMAGES

VIDEO

COMMENTS

Understand the reasons and timing for reverse mortgages being assigned to HUD, and discover essential steps to take for managing your reverse mortgage effectively.

The HECM is the FHA's reverse mortgage program that enables you to withdraw a portion of your home's equity to use for home maintenance, repairs, or general living expenses. HECM borrowers may reside in their homes indefinitely as long as property taxes and homeowner's insurance are kept current.

Reverse mortgages are increasing in popularity with seniors 62 and over who have equity in their homes. A reverse mortgage enables you to withdraw a portion of your home's equity to supplement your income, or to purchase a home. There are no monthly principal and interest payments.

HUD will not accept a loan for assignment if it is in default or is due and payable. The review focuses on origination documents and ensures that there are no errors on the mortgage, that...

Most reverse mortgages today are Home Equity Conversion Mortgages (HECMs), which are federally insured by the U.S. Department of Housing and Urban Development’s (HUD) Federal Housing Administration (FHA). This guide covers typical features and requirements for HECM reverse mortgage loans.

Reverse mortgage counseling assists clients who seek to convert equity in their homes into income that can be used for any purpose such as, but not limited to, ongoing property taxes, property insurance, home repairs and improvements, medical costs, and living expenses.